I. Policy Analysis

(1) Common Support from Domestic Policies

Driven by China's "dual carbon" goals, the hydrogen energy industry planning continues to improve, encouraging various technological approaches for electrolyzers. For instance, the "Medium and Long-Term Plan for the Development of the Hydrogen Energy Industry (2021-2035)" explicitly supports the R&D and demonstration applications of electrolyzer technologies. Various localities have also introduced supporting policies such as subsidies and priority access to green electricity, promoting the implementation of green hydrogen projects and creating a policy environment for the development of alkaline, PEM, AEM, and SOEC electrolyzers.

(2) Policy Differences by Technological Approach

1. Alkaline Electrolyzers:With a high level of technological maturity, domestic policies focus on promoting large-scale applications. In wind and solar power-to-hydrogen projects, priority is given to supporting demonstrations of alkaline electrolyzers with cost advantages, such as large-scale wind and solar power bases paired with green hydrogen projects, which require indicators like the proportion of alkaline electrolyzers to consolidate their market foundation.

2. PEM Electrolyzers:Domestic policies focus on breaking through "bottleneck" technologies, providing special subsidies for the R&D of PEM electrolyzers with high current density and long lifespan, encouraging enterprises and universities to collaborate on core components such as membrane electrodes and bipolar plates, and promoting their pilot applications in distributed hydrogen production and green hydrogen coupling scenarios (such as hydrogen refueling stations).

3. AEM Electrolyzers:Still in the technological exploration phase, domestic policies primarily focus on scientific research support. Through special projects for hydrogen energy technological innovation, they support the R&D of key materials for AEM electrolyzers (such as anion exchange membranes), encourage the construction of pilot production lines, and cultivate technological reserves.

4. SOEC Electrolyzers:Belonging to cutting-edge technologies, policies emphasize the integration of "zero-carbon hydrogen production + energy storage," supporting demonstration projects for cross-seasonal energy storage that couple SOEC with renewable energy. They provide funding for research topics such as high-temperature electrolysis system integration and waste heat utilization, laying out the future energy system.

(3) International Policy Trends

Overseas, countries like the EU and the US primarily focus on hydrogen energy supply chain security and decarbonization goals: The EU's "Hydrogen Strategy" imposes carbon footprint requirements on the entire industry chain of electrolyzers, with subsidies favoring efficient and low-carbon technologies such as PEM and SOEC. The US's IRA Act incentivizes green hydrogen projects through tax credits, with PEM receiving subsidy preferences due to its suitability for distributed scenarios. Meanwhile, both Europe and the US are promoting technological breakthroughs in SOEC and other technologies through international cooperation, such as hydrogen energy research initiatives, squeezing the technological adaptability competition for China's electrolyzers to go global.

II. ALK Electrolyzers

(1) Overview

(2) Market Analysis

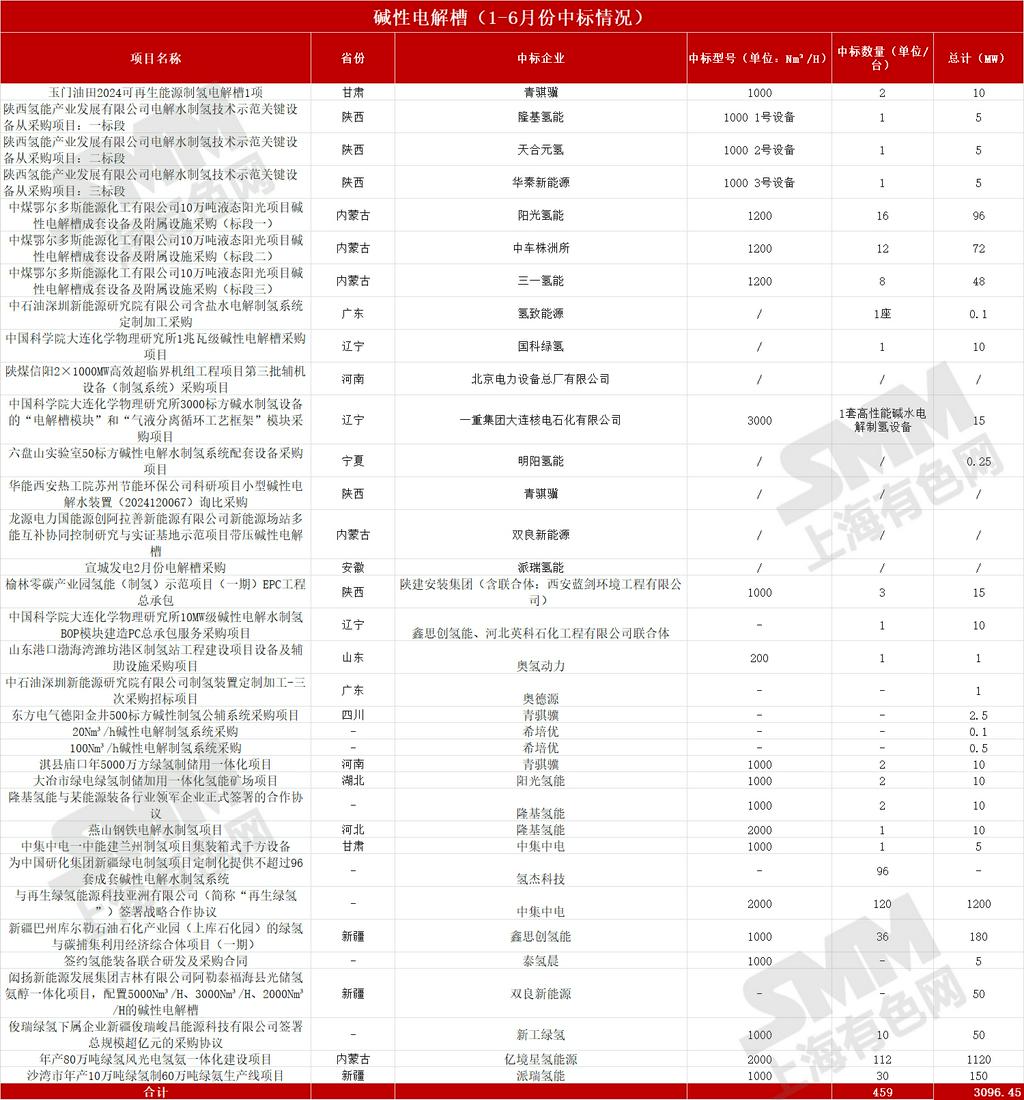

1. Domestic Market:According to publicly available statistics compiled by SMM, in the first half of 2025 (January-June), there were 35 awarded projects for alkaline electrolyzers, with a total of 459 alkaline electrolyzers awarded, amounting to 3096.45 MW. Overall, the awarded projects for alkaline electrolyzers are predominantly large-scale, dominating green hydrogen projects on a large scale, such as large-scale wind and solar power-to-hydrogen bases and coal-fired power coupling decarbonization projects. Leveraging cost advantages of approximately 0.8-1.2 yuan/W and mature technology, it commands over 80% of the market share. Demand is concentrated in regions rich in wind and solar power resources, such as Inner Mongolia and Ningxia, for applications in green hydrogen chemical engineering and coal-to-hydrogen substitution scenarios.

2. Overseas Markets:China, with its complete industry chain and cost advantages (30-40% lower than Europe and the US), is competitive in overseas low and mid-end markets, such as Southeast Asia and Middle Eastern wind and solar power hydrogen production projects. However, due to restrictions like "carbon tariffs" and "technical barriers" imposed by Europe and the US, access to high-end projects like "EU green hydrogen certification projects" is difficult. Exports are mainly dominated by large equipment integrators, focusing on cost-effectiveness.

(III) Future Outlook

1. Evolution of Technical Routes:Alkaline electrolyzers will remain the market's mainstay in the short term (3-5 years), with technology upgrading towards "high current density (≥5kA/m²), long lifespan (>50,000 hours), and intelligent operation and maintenance," consolidating the advantage of large-scale hydrogen production after cost reduction. In the long term, due to the iteration of PEM and AEM technologies, it may gradually shift towards "stock replacement + ultra-large projects."

2. Market Prospects:"Maturity + Scale Growth." Domestic demand in China is expected to grow by 15-20% annually from 2025 to 2030, while overseas markets (mainly focusing on developing countries) are expected to grow by 25-30% annually. However, profit margins will narrow with competition, and enterprises will need to rely on "scale + operation and maintenance services" for profitability.

III. PEM Electrolyzers

(I) Overview

(II) Market Analysis

1. Domestic Market:According to publicly available statistics from SMM, there were 9 awarded PEM electrolyzer projects from January to June 2025, with a total of 13 PEM electrolyzers, amounting to 14.55MW. Demand is focused on scenarios requiring "high purity, small volume, and flexible hydrogen production," such as distributed green hydrogen projects like hydrogen refueling station support in Shaanxi and Qinghai, and industrial park demonstrations. Due to reliance on imported core components, costs are high (approximately 2-3 yuan/W), but they are irreplaceable in scenarios with high water quality requirements and limited space (such as electronic-grade hydrogen). The market is growing rapidly (with a YoY increase exceeding 50% from January to June).

2. Overseas Markets:Overseas markets are dominated by Siemens Energy and ThyssenKrupp. Chinese enterprises lag significantly in membrane electrodes and control algorithms. Only a few enterprises, such as Hydrogen Pro, are testing the waters through "cost-effectiveness + customization" (tailored for distributed projects in developing countries), with small export scales. However, there is breakthrough potential in green hydrogen projects for small hydrogen refueling stations in the Middle East under the "Belt and Road" initiative.

(III) Future Outlook

1. Technology Roadmap Evolution: PEM electrolyzers may enter the "breakthrough phase" within 3-5 years, with the localisation rate of core components such as membrane electrodes and titanium bipolar plates increasing to 60-70%, and costs decreasing to 1.5-2 yuan/W. They will replace alkaline electrolyzers in distributed hydrogen production scenarios (hydrogen refueling stations, green electricity consumption in data centers) and high-purity hydrogen scenarios (electronics, semiconductors). In the long term, over 5-10 years, they may form a complementary pattern of "large-scale - distributed" with alkaline electrolyzers.

2. Market Outlook Projections: "Growth Phase + High Growth Rate". From 2025 to 2030, domestic demand is expected to increase by 50-60% annually, while overseas demand (distributed projects in Europe and the US) is expected to increase by 40-50% annually. Core component enterprises (membrane electrodes, bipolar plates) and high-end electrolyzer enterprises (suitable for multiple scenarios) will command high premiums and become the focus of market competition in the next 3-5 years.

IV. AEM Electrolyzers

(I) Overview

(II) Market Analysis

1. Domestic Market: According to publicly available statistics compiled by SMM, there were 4 awarded projects for AEM electrolyzers from January to June 2025, with a total capacity of 65.125 MW, indicating that they are still in the pilot stage. Due to their combination of alkaline cost potential and some advantages of PEM, they are being tested in small-scale green hydrogen demonstration projects such as scientific research projects, hydrogen energy laboratories in universities, and small green hydrogen factories. Demand is scattered, and enterprises aim for technology verification, with no large-scale orders formed yet.

2. Overseas Market: The overseas market is basically monopolized by European, American, and Japanese enterprises such as Giner and Topsoe. Chinese enterprises are still in the technology catch-up phase, with extremely low participation in the overseas market. They only accumulate experience through academic cooperation and small-scale sample inspections (such as sending AEM membrane materials to Europe for testing), making it difficult to form exports in the short term.

(III) Future Projections

1. Technology Roadmap Evolution: AEM electrolyzers may become a "dark horse" in 5-10 years. If breakthroughs are achieved in the service life of anion exchange membranes and electrode materials, they can integrate alkaline costs (0.8-1 yuan/W) with PEM flexibility, replacing parts of the alkaline and PEM markets in "medium-scale green hydrogen projects (10-100 MW), island/off-grid hydrogen production". This depends on the industrialization speed of core materials.

2. Market Outlook Projections: "Nurturing Phase + Technological Competition". From 2025 to 2030, the market will be dominated by "pilot orders + scientific research cooperation". Enterprises need to invest in material R&D. If breakthroughs are achieved, they will enter the "rapid growth phase"; otherwise, they may be squeezed out by PEM and alkaline electrolyzers, with market risks and opportunities coexisting.

V. SOEC Electrolyzers

(I) Overview

(II) Market Analysis

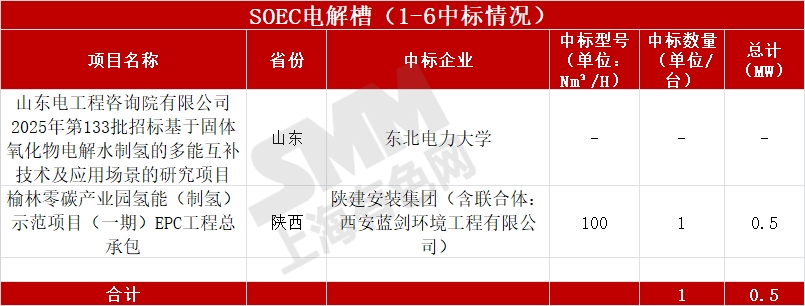

1. Domestic Market: According to publicly available statistics compiled by SMM, in the period from January to June 2025, there were 2 awarded projects for SOEC electrolyzers, with a total of 1 SOEC electrolyzer awarded, amounting to a total capacity of 0.5MW. With only 0.5MW awarded, the focus is on innovative scenarios of "green electricity + ESS + hydrogen production," such as the Shaanxi Zero-Carbon Industrial Park Coupling Project. Relying on high-temperature waste heat utilization to adapt to industrial by-product heat and solar thermal power plants, it primarily emphasizes cross-seasonal energy storage in the "electricity-hydrogen-electricity" cycle. However, the technology's maturity is low, and there is an urgent need for verification in terms of efficiency, lifespan, etc. Market demand is relatively niche, mainly for scientific research demonstrations.

2. Overseas Market: The situation for SOEC and AEM overseas is roughly similar, with European, American, and Japanese companies basically monopolizing the technology routes. Participation in overseas markets is extremely low, and Chinese enterprises are still in the technology catch-up phase.

(III) Future Expectations

1. Evolution of Technology Routes: SOEC electrolyzers represent a "potential track" spanning over 10 years. If issues such as high-temperature sealing and material corrosion (lifespan > 10,000 hours) are resolved, they can rely on multi-energy coupling of "electricity-hydrogen-heat" (such as solar thermal power plants + SOEC electricity and heat storage) to explode in scenarios of cross-seasonal energy storage and industrial by-product heat utilization, becoming a key technology for the "zero-carbon energy system." However, commercialization is difficult in the short term.

2. Market Outlook Expectations: "Incubation period + long-term layout." From 2025 to 2030, the focus will be on "demonstration projects + policy topics," suitable for central state-owned enterprises and scientific research-oriented enterprises to lay out technology reserves, waiting for the "energy revolution" opportunity after the technology matures in 10 years. Revenue contribution is difficult in the short term.

Conclusion

Overall, due to differences in policy support, market demand, and technology maturity among various electrolyzer technology routes, the landscape presents as "alkaline electrolyzers stable, PEM electrolyzers advancing, AEM electrolyzers speculative, and SOEC electrolyzers hidden." Enterprises need to accurately position themselves in technology evolution and market demand to gain an advantage in the hydrogen production equipment track.

(All the above data are sourced from publicly available statistical data.)